When companies invest in other companies, the accounting treatment depends on how much influence the investor has.

One of the most commonly misunderstood — yet frequently tested — approaches is the Equity Method.

In this article, I will explain the equity method step by step, using logic, intuition, and practical examples rather than pure theory.

What Is the Equity Method?

The equity method is an accounting method used when an investor has significant influence over another company, but does not have control.

Under this method:

- The investment is recorded as a single line item on the balance sheet.

- The investor recognizes its share of the investee’s profits or losses, regardless of whether cash is received.

Think of it this way:

You are not just a passive shareholder — you are economically involved.

When Is the Equity Method Used?

In practice, the equity method is generally applied when the investor owns between 20% and 50% of the voting stock of the investee.

However, percentage alone is not everything.

The key concept is significant influence, which may exist if:

- The investor has representation on the board of directors

- The investor participates in policy-making decisions

- There are material intercompany transactions

- Management personnel are shared

If significant influence exists, equity method accounting is required under US GAAP.

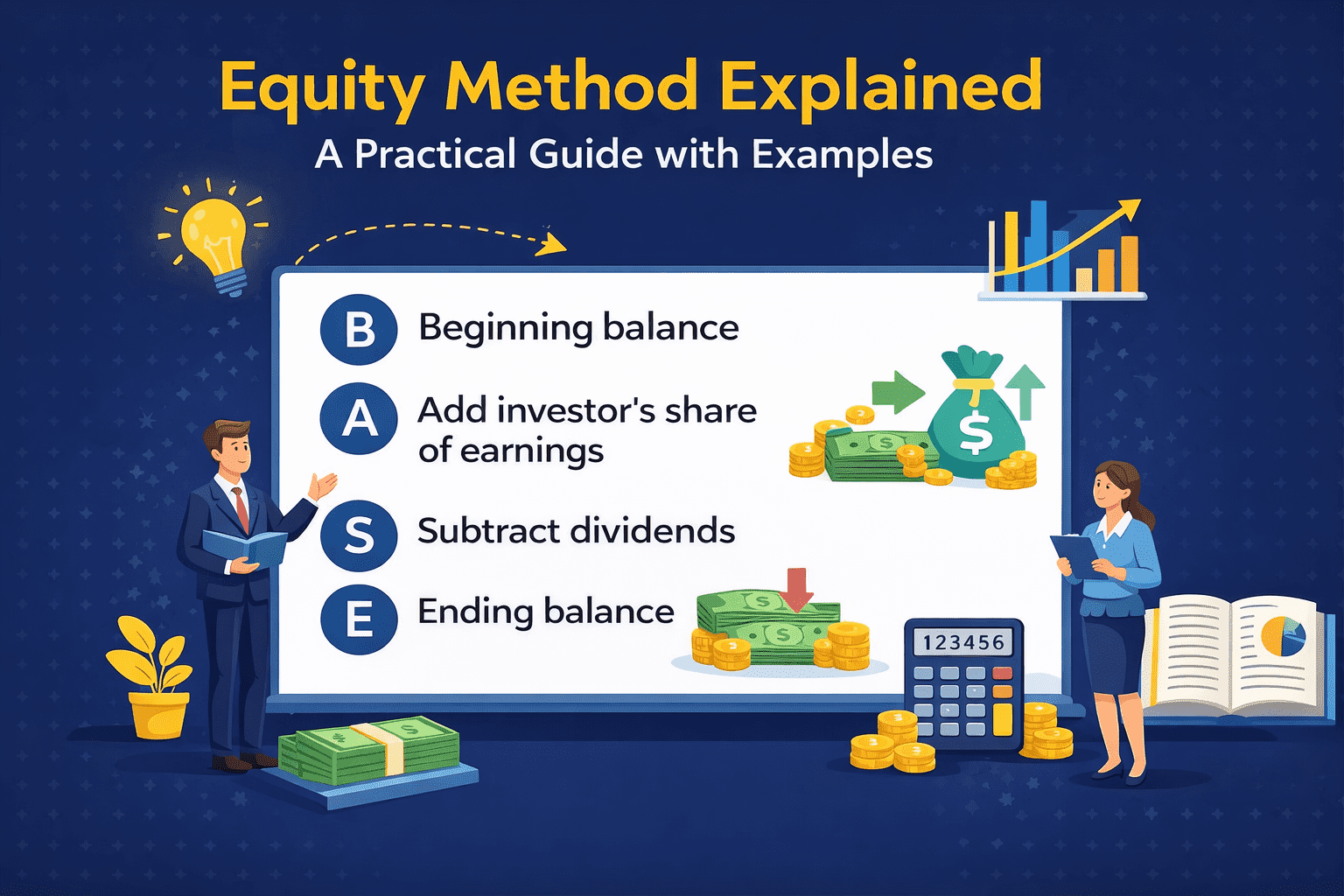

The Core Idea: Treat the Investment Like a Bank Account

The easiest way to understand the equity method is to think of the investment as a bank account.

This leads to a very important framework often summarized as BASE:

- Beginning balance

- Add investor’s share of investee’s earnings

- Subtract dividends received

- Ending balance

This framework explains almost everything you need to know.

Initial Recognition

When the investment is first acquired, it is recorded at cost.

Example:

A company acquires a 30% interest in another company for $300,000.

Journal entry:

Investment in Associate 300,000

Cash 300,000

At this point, the investment account simply reflects what you paid.

Recognizing the Investee’s Profits

Here is where the equity method becomes unique.

If the investee earns income, the investor must recognize its proportionate share of that income — even if no cash is distributed.

Example:

- Investee’s net income: $100,000

- Investor ownership: 30%

Investor’s share:

100,000 × 30% = 30,000

Journal entry:

Investment in Associate 30,000

Equity Income 30,000

Key point:

Income is recognized when earned, not when cash is received.

Dividends Are Not Income

This is one of the most common mistakes.

Under the equity method, dividends are not income.

They are treated as a return of investment.

Why?

Because the income was already recognized when the investee earned it.

Example:

The investor receives $10,000 in dividends.

Journal entry:

Cash 10,000

Investment in Associate 10,000

Notice:

- No income is recorded

- The investment account decreases

This mirrors a bank withdrawal — you are not earning money, you are taking it out.

Purchase Price vs. Fair Value of Net Assets

Often, the price paid for an investment is different from the investor’s share of the investee’s book value.

This difference usually arises because:

- Certain assets or liabilities are recorded at amounts different from fair value

- The investor paid a premium for future benefits (goodwill)

Under the equity method:

- The difference is embedded in the investment account

- Fair value adjustments related to depreciable or amortizable assets reduce equity income over time

- Goodwill is not amortized under US GAAP, but tested for impairment indirectly

Losses Under the Equity Method

If the investee incurs a loss, the investor must recognize its share of that loss.

Example:

- Investee loss: $50,000

- Ownership: 30%

Investor’s share:

15,000 loss

Journal entry:

Equity Loss 15,000

Investment in Associate 15,000

The investment account decreases accordingly.

How the Investment Appears in Financial Statements

- Balance Sheet:

A single line item called Investment in Associate (or similar) - Income Statement:

A single line item called Equity in Earnings of Investee

There is no consolidation of revenues, expenses, or assets.

Equity Method vs. Other Methods (Quick Comparison)

- Less than 20% ownership

→ Fair value or cost method - 20% to 50% ownership

→ Equity method - More than 50% ownership

→ Consolidation

Understanding this progression is critical for both practice and exams.

Final Takeaway

The equity method reflects economic reality rather than cash movement.

If you remember just one sentence, let it be this:

Under the equity method, profits are income, dividends are not.

Once this logic is clear, the journal entries and calculations fall into place naturally.